AT&T (New York Stock Exchange: T) It has been a popular dividend stock for many years due to its relative stability, name recognition, and high return. The company is Dividend Aristocrat – which means it has raised its annual dividend for at least 25 consecutive years – and is currently producing 6.8%.

However, AT&T has become a very complex company due to its history of acquisitions. Management’s track record of making good acquisitions and consolidating well is shaky at best. This makes AT&T’s high debt burden particularly risky. On the contrary, Lumen Technologies (NYSE: LUMN) It offers a higher return despite having a lower dividend payout ratio and simpler business that carries less risk to investors. This makes Lumen a more attractive dividend stock.

Strategic confusion reigns at AT&T

AT&T has made two huge acquisitions since 2015. First, it acquired satellite broadcasting provider DIRECTV in 2015 with a total value for the enterprise of approximately $ 67 billion. Three years later, the acquisition of Time Warner closed, with the entertainment giant being paid more than $ 104 billion. These two deals played a major role in increasing AT&T’s debt burden. At the end of the fourth quarter, AT&T debt totaled $ 158.9 billion, down modestly from $ 163.1 billion at the start of 2020.

Image source: Getty Images.

In hindsight, the DIRECTV deal was a fatal mistake, although AT&T management never admitted it. The position is completely closed as the wire cutting trend accelerates. AT&T has suffered one of the worst subscriber losses to the pay-TV industry in the United States in recent years.

AT&T is now close to selling a large stake in DIRECTV (excluding the relatively small satellite business in Latin America) with a valuation of barely over $ 15 billion, according to The Wall Street Journal. This sounds like nothing more than financial engineering. AT&T only wants DIRECTV off the books – although selling a portion of the business at a low rating will reduce the free cash flow for a relatively small cash injection.

The acquisition of Time Warner appears to have been slightly more successful. John Stankey, CEO of AT&T, and new WarnerMedia president, Jason Keeler, has overhauled the media company’s business model, focusing all of its resources in building the HBO MAX as Netflix competitor. This hurts profitability in the near term. Unfortunately, HBO MAX got off to a tough start due to confusing brands as one of the many variants of HBO. After more than six months, it has only 12.6 million subscribers. That’s a fraction of HBO’s subscriber base, although the HBO MAX is a free upgrade to the first. On the contrary, Walt DisneyDisney + launched last November and already has 86.8 million subscribers globally.

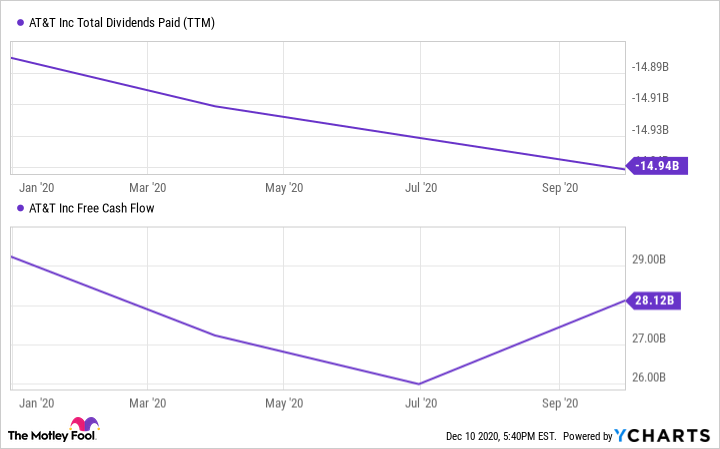

AT&T will have to invest heavily in HBO MAX to get the scale right. If it does not grow enough to offset the declining portions of AT&T business, free cash flow may continue to decline from an expected $ 26 billion or so in 2020 and 2021. This, in turn, could jeopardize dividends, which cost about $ 15 billion. General, put AT&T dividend payout ratio in the range of 57% to 58% (as a percentage of free cash flow).

AT&T free cash flow versus dividend payments. Data by YCharts. TTM = last 12 months.

There is a better alternative

By contrast, Lumen Technologies – formerly known as CenturyLink – pays a quarterly dividend of $ 0.25 per share. This gives it a 10% return, and it easily beats AT&T. On top of that, Lumen typically generates at least $ 3 billion in free cash flow annually, so the $ 1.1 billion it pays out in dividends represents a much lower payout ratio of 40%. The combination of a high return and a low payout ratio makes it more interesting Distributed shares directly.

To be fair, Lumen’s debt burden is higher than AT&T for EBITDA (EBITDA). However, thanks to its low dividend yield, it was able to write down quickly. It ended the fourth quarter with $ 32.6 billion in debt, down from $ 36.1 billion at the start of 2019.

In between Lumen’s efforts to reduce leverage and refinance, interest expense is on track to decline to $ 1.7 billion this year from $ 2.2 billion in 2018. Annual interest expense is likely to continue declining, ending between $ 1.2 billion and $ 1.3 billion by 2023. This will support the continued strength of free cash flow and potentially allow Lumen to Start increasing their profits In a few years.

There is a clear winner

AT&T’s wireless business and its fiber broadband service are two stable sources of profit supporting its huge profits. However, AT&T also has significant exposure to declining industries such as pay TV. Its haphazard response to changes in how people consume content does not inspire confidence that the company can maintain (let alone grow) the profitability of its entertainment business.

Lumen is also exposed to declining markets such as legacy voice service and DSL internet. However, instead of pumping resources to try to revive the ailing business, management is focusing on leveraging the vast fiber network to take advantage of the growing demand for low latency internet connections.

With higher dividend yield, better dividend coverage, and lower operating risk in the business, Lumen Technologies is a much more attractive stock than AT&T.

“Explorer. Devoted travel specialist. Web expert. Organizer. Social media geek. Coffee enthusiast. Extreme troublemaker. Food trailblazer. Total bacon buff.”